Current Price

$319.60

ROE (TTM)

60.35%

Free Cash Flow (TTM)

$21.19B

Trailing P/E

27.2x

Revenue (TTM)

$43.03B

Market Cap

$602B

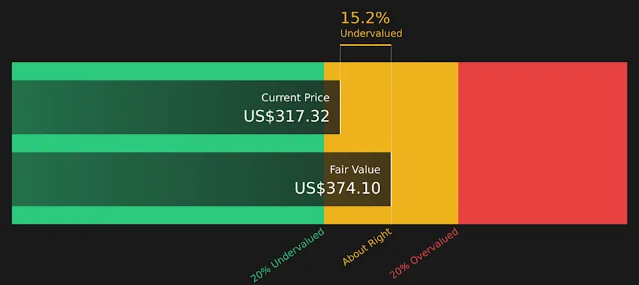

Visa clears all three hard screens — trailing ROE at 60.35%, $21.19B in annual free cash flow, and a forward P/E of 22.4x — while trading 12% below its 52-week high. Today's pick examines whether the macro-driven pullback makes this the right entry for a quality compounder.

| Company | ROE (TTM) | P/E (TTM) | P/FCF | FCF Margin |

|---|---|---|---|---|

| Visa (V) | 60.4% | 27.2x | 27.8x | 49.2% |

| Mastercard (MA) | 232.1%* | 27.3x | 23.4x | 52.4% |

Add more perspectives or context around this Post.